Measuring Uncertainty in Stock Markets

Jorge M. Uribe, Helena Chuliá and Montserrat Guillen

We propose a daily index of

time-varying financial uncertainty. The index is

constructed after first removing the common variations

in the series, emphasizing on the difference between

risk (expected variation) and uncertainty (unexpected

variation).

The complete paper can be found in:

The complete paper can be found in:

- Chuliá, H., Guillen, M., and J.M. Uribe (2016). Measuring Uncertainty in Stock Markets, . International Review of Economics and Finance, 48, 18-33.

DATA DESCRIPTION

We use 25 portfolios of stocks belonging to the NYSE, AMEX, and NASDAQ, sorted according to size and their book-to-market value, as provided by Kenneth French on his website

Methodology

The construction of our

uncertainty index consists of two steps. First, we

remove the common component of the series under study

and calculate their idiosyncratic variation. To do

this, we filter the original series using a

generalized dynamic factor model (GDFM). Second, we

calculate the stochastic volatility of each residual

in the previous step using Markov chain Monte Carlo

(MCMC) techniques. Then, we average the series,

obtaining a single index of uncertainty for the stock

market

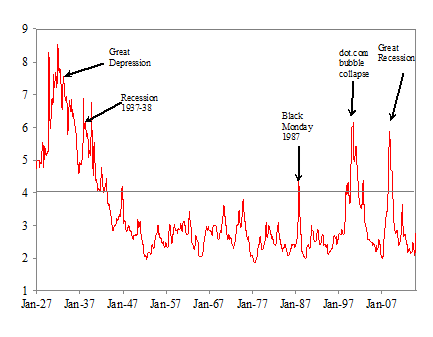

Financial Uncertainty Index

Figure 1: US Uncertainty Index:

Jan-06-27 to Sept-30-14. Grey areas correspond to NBER

- Universitat de Barcelona - Last Updated: 10-23-2016